Egypt, April 6th 2025

Things were getting better until "Liberation Day " !

Welcome to MENA MARKET LAB !

We aim here to bring you regular updates on factors and events impacting financial markets in the Middle East and North Africa region with an accent on foreign exchange and rates.

We also aim to bring reflections on certain topics and subjects, close to recent events, which we think are worth stopping on .

Thank you for your attention

Things were getting better ! Until "Liberation Day " !

Hard to describe ! We all read that France’s leader of the far right party Rassemblement National and a few others have been convicted of embezzlement and banned from taking part in elections. She is not the first one, there is a long list of French politicians and former presidents who have been caught for similar crimes. Obviously she claims she is the target of a witch hunt and this is the execution of democracy. Her supporters have threatened the judge on the case. Also familiar. She has received the support of Putin, Trump, Orban, Salvini and other various liberal-democrats and human right defenders. She even compared herself to Martin Luther King ! Really ? Russia has provided financial support for her party in the past so it is also interesting that she compares herself to Alexei Navalny , an opposition leader in Russia , jailed under Putin and who died in mysterious conditions in an Artic penal colony.

Now,

After Liberation Day in the US on Thursday, fundamental data released after for other countries and even the US seemed completely irrelevant. Only President Trump noticed the great NFP numbers on Friday.

For Egypt, we had the release of the non-oil sector PMI and it was a bit disappointing: it fell into contraction area again after just two months above 50. A deterioration in business activity saw the index fall to 49.2 in March from 50.1 in February. The construction sector remains robust and inflation pressures are easing. The decline was mainly driven by lower demand for local and international orders.

As David Owen, Senior Economist at S&P Global Market Intelligence ( they publish the index) wrote , “ part of this softening was linked to a weaker dollar , which continues to be influenced by evolving US trade policies. This uncertainty has dampened business expectations”.

The index was published before the chaos unleashed by the WH.

The IMF released the 1.2 bn $ tranche of the EFF after the approval of the 4th review.

The European Parliament has adopted the Macro-Financial Assistance program to Egypt ( and also to Jordan ) by 452 votes in favour and 182 against, 40 abstentions. This Assistance will provide 4 bn euros in loans. This was initiated a year ago .1 bn euros were already released late 2024.

Market wise,

There will be what happened before Liberation Day and after.

Up to April 3rd, the spot market was quite stable, dealing around 50.60. The NDF curve dropped as markets were expecting rate cuts at next MPC meeting on April 17th. As low as 58.45 mid for the 1 year NDF.

Primary issuances : March was a big month as over 1.3 trillion EGP ( 26 bn $) Worth of bills were maturing , outcome of last year’s devaluation and huge appetite of investors for high yield paper afterwards.

The Ministry of Finance had an adjusted issuance program of 760 bn EGP for March . 857 bn were accepted directly at the auctions as investors were busy buying treasury bills to take advantage of high yields before the CB starts to cut rates following the good inflation numbers of March 10th.

Scrounging into EGX data ( you have to check each maturity to verify if the amount differs from what the CBE declared accepted !) , one can find that there are another 680 bn EGP that have been issued as Private Placements. So all in all , success, 1.3 trillion EGP matured and about 1.5 trillion issued.

April would have been quieter as only 250 bn EGP were/are due to mature.

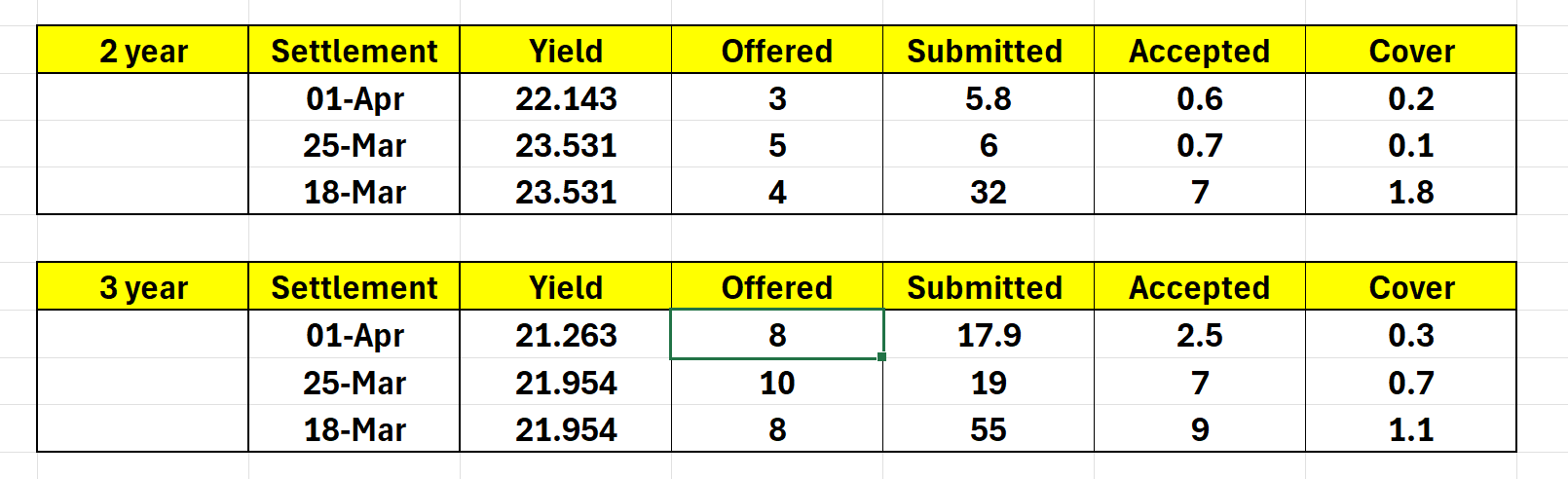

We could observe though that whereas the last auctions of March had a decent cover ratio ( 1.5 for March 18th settlement and 1.24 for March 18th settlement ) , it dropped to 0.3 for Settlement April 1st and even lower for today’s auctions of 91 and 273 days papers with yields rising again as is shown in table below . The 3month rose back to 28.244 from 27.35 two weeks back.

Shown differently below , grouping by paper maturity instead of settlement date.

And for the bond side :

The secondary market was kept very busy in March: to see a higher secondary market volume, one has to go back to March 2024 following the last devaluation : 1.66 trillion EGP dealt in March 2025 compared to 1.787 in March 2024.

But March 25 is 80 % above February’s volume, true a quiet month ( January was 1.4 trillion).

Whereas Foreigners were net sellers in February ( 1.4 bn $ equivalent) , they were quite aggressive net buyers in March , 3.7 bn $.

Arab counterparties continued to buy : a further 630mio $ in March bringing the total to 1.7 bn $ since the beginning of 2025.

For note , local equity markets were down with the EGX30 showing a loss of 3.34 % today.

Now before we go to what happened past few days, it is worth mentioning a very good analysis that was made on Egypt ( dated April 2nd) by a top US institution and the perspective for rate cuts.

Some observations to be made on the perceived behaviour of the CBE :

· They have shifted from an expectation-based forecast to a data-driven approach : everybody was expecting the inflation to drop sharply in February including the CBE but they needed to see the print.

· Concerns that Egyptians are still very cautious and look at prevailing inflation rather than forward looking.

· The CBE is firmly set on avoiding FX instability.

Egypt’s economic growth potentials are still unrealized. The IMF has been regularly revising down GDP growth forecasts. The non-oil sector PMI shows it is struggling to remain above 50. The energy sector hasn’t helped for the past year.

Potentially positive , falling energy prices if they were to persist would lower the price increases the government needs to perform to bring retail energy prices to cost, so helping inflation lower.

High rates are a drag on the economy : high borrowing costs, lower consumption; real interest rates at record levels, over 15 %.

Plus the fact that interest payments on the debt capture over 75 % of the State ‘s revenues . And a rising budget deficit even though lately the primary surplus was at record level.

Finally, the higher the real rates, the more risk on debt sustainability and higher debt ratios.

That institution was seeing the CBE cutting rates by 800 bps in Q2 2025 and by over 1200 points in the next 12 months.

To the question : would too low rates spook investors , geopolitical and economic events have a bigger impact on inflows and outflows than the level of nominal and real interest rates. The largest recent outflows were on those events : 2011 Revolution, Covid, Ukraine conflict and inflows , IMF programs !

All this is very good and interesting but it didn’t factor Trump.

Thursday surprisingly local markets were still a bit quite with spot unchanged at 50.60.

But all changed the next day, closed in Cairo though.

· The yield on Egypt’s USD bonds jumped higher , example the yield on the 8 7/8 % May 29 2050 rose from11.6 % to 12.5 %.

· 1 year NDF jumped to 60.40 from 59.

· Today the spot rose to a high of 51.26 before setting at 51.17 from 50.60 on Thursday with an exceptionally large volume of 1.15 bn $ for a Sunday.

· A few offshore clients were to be found behind their desks today : October 2027 local bond dealt at 24.70 % from 24 % on Friday . The last 2yr and 3 yr auction would put the yield around 21.75 %. As for the bills, bids shown in markets are fully 1.25 % above last. Respectively for the 3m, 6, 9m and 1year : 29.25 %, 28.25 % , 27.50 % and 26 %.

Even though much needs to be done locally in terms of structural reforms and divestments to improve the economy, it seems that whenever things start to get better, some big external factors come to rock the boat : pandemic, conflict in Ukraine, war in Gaza and now the chaos created by President rump’s favourite word, tariffs.

In front of this chaos, it is all too natural that quite a few will consider trimming their exposure even more so after having increased it recently with the perspective of soon to come aggressive rate cuts.

Hard to say how the situation will evolve in the coming days with Trump’s unpredictability but if FX outflows continue aggressively over the next days, that will certainly reduce the appetite for the CBE to cut rates at next meeting on April 17th.

Stay put !

Thank you

DC