Egypt, May 12th 2025,

CPI higher ; PMI and Macro data disappoint ; IMF in town for the 5th review ; keep your Treasury bills though !

Welcome to MENA MARKET LAB !

We aim here to bring you regular updates on factors and events impacting financial markets in the Middle East and North Africa region with an accent on foreign exchange and rates.

We also aim to bring reflections on certain topics and subjects, close to recent events, which we think are worth stopping on .

Thank you for your attention !

CPI higher ; PMI and Macro data disappoint ; IMF in town for the 5th review ; keep your Treasury bills though !

First,

Let’s not join the crowd of those happy to bash on experts, specialists, economists of all kind. It is true though for example that 3 years ago, after Putin launched its special military operation in Ukraine and the following harsh sanctions, most predicted that Russia’s economy would shrink by 10 to 15 % and the currency to collapse.

It did go down by ..1.5 % in the first year and then recovered nicely showing growth for the past two years above 4 % ; the currency initially weakened and then recovered stronger. Most didn’t see that Putin had been readying Russia for over 10 years.

Today, many forecasts the US economy to go into recession, the dollar to collapse and the external world to dump trillions of US debt. If only there was a unified European debt market. So the reality again might be more nuanced. If Taiwan liquidates its 2 trillion dollars of assets, what will they buy instead ? gold, crypto, Melania coins ? Who said “ if I owe a bank one hundred thousand dollars , it is my problem, if I owe them 1 billion dollars , it is their problem ! “ There you go !

Now,

Few facts and numbers :

· Egypt’s net international reserves continue to grow , at a measured pace : they rose to 48.143 bn $ at the end of April from 47.757 bn $ in March and 47.393 in February.

· NFA, the Net Foreign Asset position of the banking sector surged in March to 15.08 bn $ from 10.18 bn in February, a 4.9 bn $ jump. The 4th EFF tranche ( 1.2 bn $ ) was paid in early April so that would not impact but the new facility of 1.3 bn $ ( RSF , Resilience and Sustainability Facility ) most likely. For the rest of the increase, we see customers’ fx deposits up by 800mn $ . The rest is a bit unclear. Could be remittances or the CBE repaying deposits placed with them. There was some decent interest from offshore investors after the CPI’s drop in March as seen from the secondary market but there were also large amounts of 1 year bills maturing in March and no obvious signs of FX activity supporting it.

· The CBE reported this week the Balance of Payments ( BOP) for the first half of Fiscal Year 2024/25 : the current account deficit widened to 11.1 bn $ from 9.6 bn $ a year ago . For calendar year 2024, the C/A deficit doubled to 22.3 bn $ from 12.6 bn $, reaching 6.2 % of GDP. Without going into too much details ( all figures below for H1 FY 2024/25 ) :

* The trade deficit rose by 47.4 % to reach 27.5 bn $ while services saw its surplus shrink by 21.2 % to 7.2 bn $.

* The oil trade deficit increased by 53.3 % to 9.7 bn $ : higher gas imports, lower crude exports.

* Suez Canal receipts down by 62.3 % to just 1.8 bn $ ( from 4.8 bn).

* On the positive side, remittances up by 80.7 % to 17.1 bn $ ;

* Tourism revenues up by 12.4 % to 8.7 bn $.

* One of the leading US Investment houses expects FDI inflows to remain strong, around 15.5 bn $ in 2025 on the back of oil and gas investments ( are prices high enough to justify it ? ) and greenfield investments in the wider economy. They also target 12 bn $ this year in portfolio inflows , 4.5bn in new external issuances and 7.5bn in local bill/bond : the maximum net exposure( net of collateral ) of offshore investors was around 18/20 bn $ ; at the end of January , it was 15.4 bn $ as reported by the CBE just for bills : so notwithstanding February to April ( February and April, outflows; March, inflows; can’t really quantify the primary side for now ) so it seems there isn’t quite enough room for 7.5 bn $. But all in all, they expect that the financing requirements for 2025 to be met and with some extra ( so higher FX reserves and higher NFAs)

· Inflation, the annual urban CPI was released yesterday morning with a small acceleration to 13.9 % in April from 13.6 % in March. Month on month, prices were up 1.5 %. Fuel price increases are one of the main reasons for the higher reading. Some were expecting a higher number due to 15 % hike in fuel pump prices and 30 % in gas. The core CPI recorded 10.4 % in April from 9.4 % in March with a 1.2 % m/m increase in April.

· Egypt’s PMI dropped again in April to 48.5 from March 49.2. The surge above 50 early this year ,which is a sign of economic expansion, was brief. Output and new business orders are lower on declining consumer spending , affecting employment levels. Egypt is still struggling to get some sustained momentum.

· It is always a bit of a struggle to explain how the GDP is growing by 3 to 4 % while the PMI is showing a contraction. Part of the answer lies apparently in the fact that many businesses are getting incorporated in official statistics from the parallel economy. This is shown partly by a 40 % surge in tax revenues without new burdens. The head of the Egyptian Tax Authority attributes the significant growth to the successful integration of informal ( parallel ) businesses into the formal economy. This is part of the structural reforms needed : as quoted from Ramy Fathallah, Head of the Egyptian-Lebanese Businessmen Association’s Tax and Finance Committee, “ .. noting a “clear and unprecedented” transformation in the relationship between taxpayers and the Authority. He attributed this shift to new policies, a refreshed mindset, and efforts to rebuild trust, which have collectively helped widen the tax base and accelerate the formalization of previously unregistered businesses “. A more efficient tax system will raise revenues without new taxes, reduce the size of the parallel economy and contribute to narrow the fiscal deficit.

· State asset sales, the announcement came as a cabinet statement that Egypt had finalized deals worth 6 bn $ under its program to sell stakes in state-owned companies. Egypt is hard pressed on this issue by the IMF.

Last , an IMF team supposedly arrived in Cairo last Tuesday and will be there until May 16th for the 5th review of the EFF program.

Market wise,

There seems to be lots of introspection and soul searching. Between the initial base-effect drop in the inflation rate, the 225 bps rate cut by the CBE last month , another of Trump’s gesticulations ( this time about requesting free passage for US Ships through the Suez Canal ) and gentle warnings by the IMF not to rush into cutting rates too fast.

Aside , it is interesting to note that even Trump’s best pals don’t always get what they wish for. Israel PM Netanyahu waited for Trump to be officially sitting in the White House to agree to a ceasefire in Gaza. In return of favours , besides keeping quiet on Bibi’s actions in Gaza, Trump agreed to a deal with the Houthis ( even praising their capacity to endure what he threw at them) but the deal doesn’t include Israel. Same with Iran, it seems the PM was made aware of the US looking to negotiate with Iran while visiting his chum in Washington . America First truly.

Back to the markets ,

· Secondary market activity is quite subdued. Offshore interest is low with April’s volume barely a quarter from March and May so far looks even slower.

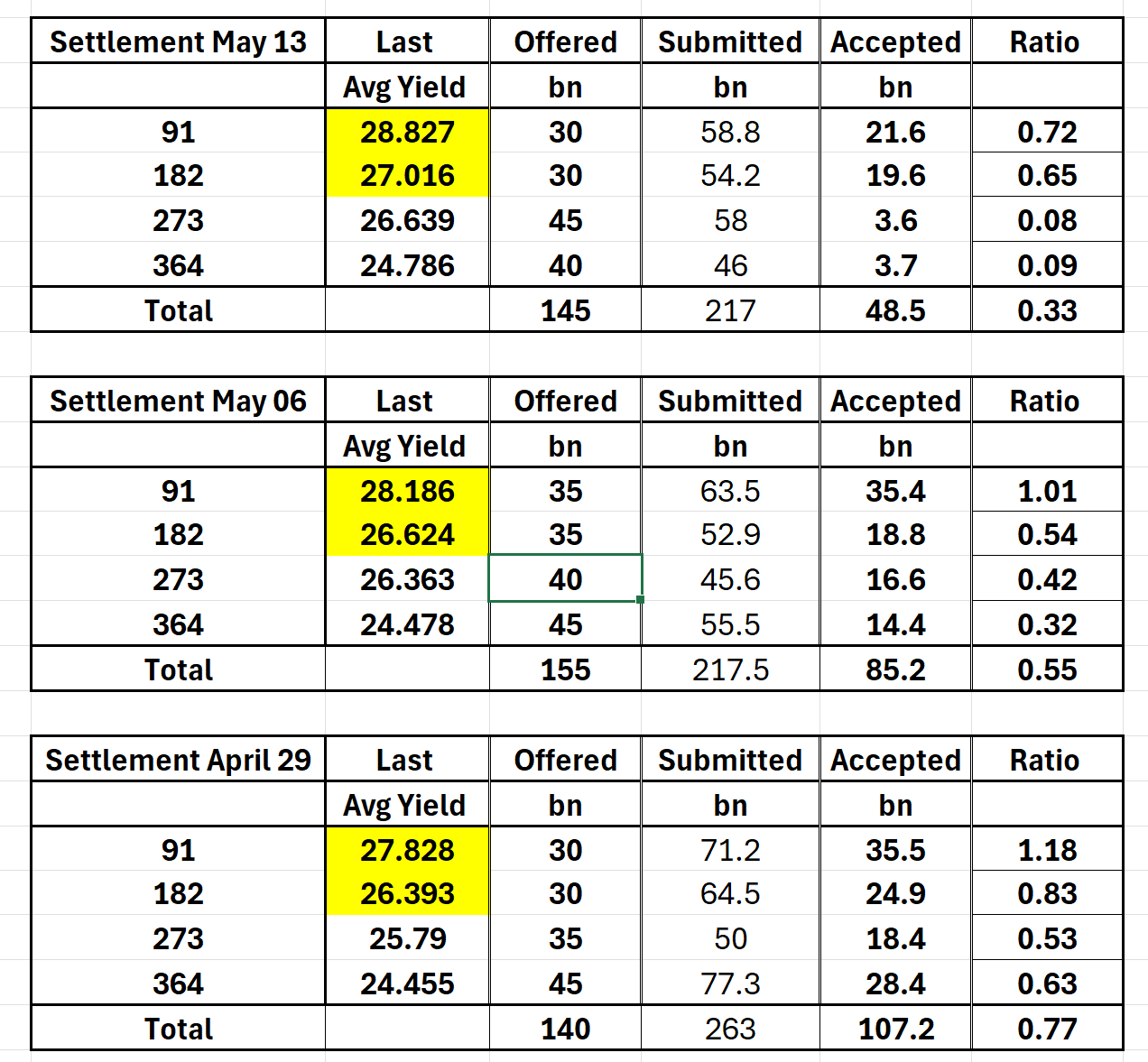

· Primary market, the bid cover ratio over the past 4 auctions has gone down steadily from 1.42 for the settlement April 15th to 0.33 for settlement May 13th and a sharp deterioration for the 9 month and 12 month papers and this with yields edging a touch higher.

· As we underlined last week, those yields are not very attractive for locals ( base rate at 25 % , no withholding tax ). Even though yields today are almost 2 % higher ( on the 91 day paper) than they were just before summer 2024, it looks a bit similar as interest in the auctions died as rates were too low : it took accepted yields to bounce back up to 29 % ( from 26 %) and above to see volumes accepted seriously increase. So if foreign investors don’t manifest themselves, the cover ratio will remain poor unless rates are more attractive.

· Spot has appreciated a bit ( as in a firmer Egyptian pound ) , trading now around 50.6050 today from 50.80 a week ago.

· On the NDF side, the curve is unchanged in outright terms , the 1 year at 59.30 mid but with higher implied yields as the spot is lower : 22.05 % mid for the 1 year ( 40 bps higher from last week ) .

So there have been some positive headlines recently, a few of them below :

· Kuwait to convert some deposits into investments ( 4 bn $),

· Qatar and Egypt agreeing for 7.5 bn $ of investments.

· Saudi Arabia given the golden service for investments and previous issues ironed out.

· EU delivering on 4 bn euros , part of a wider 7.5bn euros package.

· Tax collections increasing,

· Government announcing completion of 6 bn $ of state-owned asset sales.

· AAIB, the Asian Infrastructure Investment Bank, will provide ( agreement to be finalized in June) 300mn $ in budget support. Mrs Rania Al Mashat , Minister of Planning and Cooperation, also added that the government was working on bringing down the debt to GDP ratio from over 90 % to 80 % within a year with a combination of debt swap agreements (Kuwait, UAE and maybe Saudi ) and debt-to -equity swaps ( potentially with Germany in the energy sector and also China).

But is still missing a strong economic push. True Egypt is not a GCC country and doesn’t enjoy the same resources but most of them are entertaining strong non-oil PMI’s and solid non-oil sector growth. Even Kuwait entertained with a higher non-oil PMI of 54. Inflation’s drop to 13 % is very positive but still very high by regional standards and the overall environment is still fragile and shaky thanks to the WH.

One figure to highlight the dilemma, debt servicing is close to 50 % of the government’s spendings and debt to GDP over 90%. Wages and other compensations only account for 17 % of government spendings.

Meanwhile, even the IMF recognized that high interest rates are still needed for now to keep markets stable and so FX !

So keep those long treasury bill positions and time to book your holidays !

Thank you

DC